Como cualquier otro negocio, un proveedor de servicios financieros vende productos para ganar dinero de modo que pueda ejecutar sus operaciones y proveer sus servicios. Para comprender cómo operan los proveedores de servicios financieros, debes saber lo siguiente: cuando depositas dinero con ellos, se agrupa en un fondo compartido con el dinero de las demás personas.

Información Básica sobre Instituciones Financieras

Seguridad

El dinero en efectivo tiene mayor riesgo de robo o pérdida. El gobierno de los EE. UU. protege el dinero que depositas en el banco. Una sola cuenta está asegurada hasta $250,000 por la Corporación de Seguro de Depósito Federal [FDIC por sus siglas en inglés], y típicamente te reembolsará tus depósitos asegurados el día siguiente. Eso significa que puedes mantener tus fondos seguros sin tener que preocuparte.

Conveniencia

Se puede acceder al dinero depositado en un banco desde cualquier lugar, por el web, un ATM o con una llamada al departamento de servicio al cliente de tu banco. Con una cuenta de banco, puedes arreglar que tu empleador deposite tu cheque de pago directamente en tu cuenta, haciendo el pago más fácil y más rápido.

Hacer presupuestos.

La revisión de un estado de cuenta bancaria, un registro del saldo en tu cuenta bancaria y las cantidades que se han pagado y sacado en ella, hace más fácil el manejar tus finanzas y seguir un presupuesto. Con un estado de cuenta bancaria vas a saber exactamente a donde va tu dinero, si va hacia un pago por un auto o una noche con amigos.

Ganando Más Dinero

La banca te permite ganar dinero con tu dinero. Suena demasiado bueno para que sea verdad, pero con el interés puedes ganar simplemente por depositar fondos en una cuenta. El banco te paga un porcentaje de interés sobre el saldo, y se añade directamente a tu cuenta cada mes.

Tutor Bancario

Para administrar tu dinero sabiamente, deberás saber cómo leer y completar la documentación relevante. Estos breves tutoriales te guiarán a través de algunos de los artículos más utilizados.

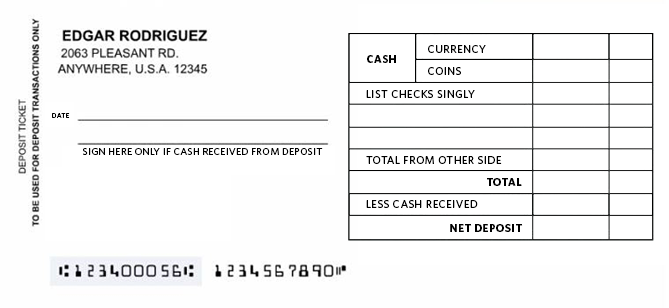

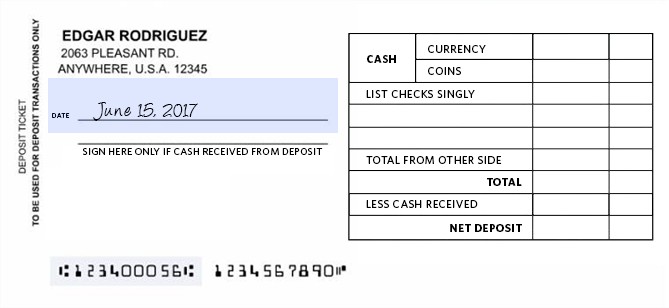

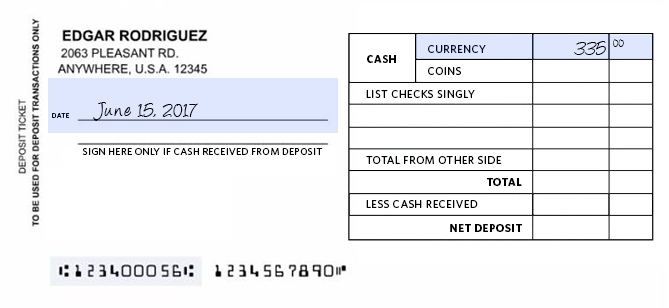

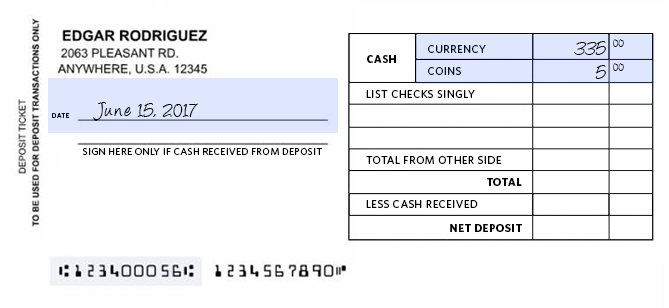

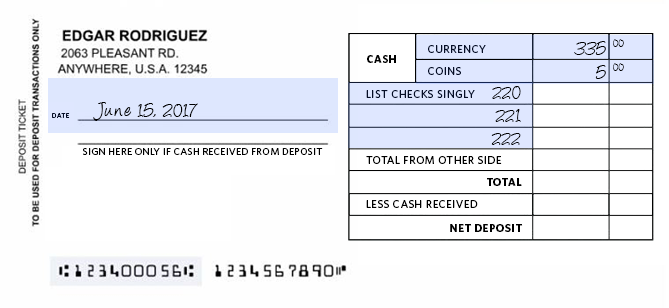

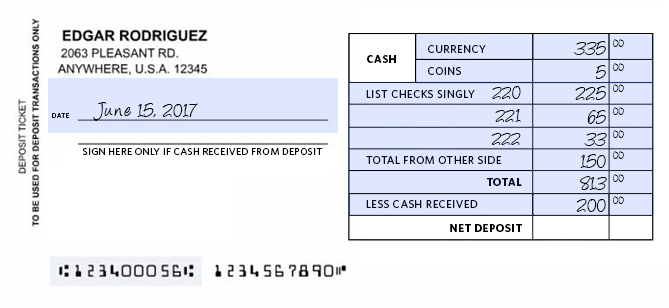

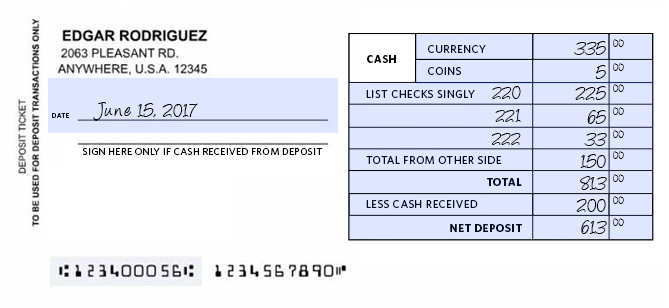

Making a Deposit

You have to deposit money in your bank account if you want to take it out. This tutorial will show you how to fill out a deposit slip.

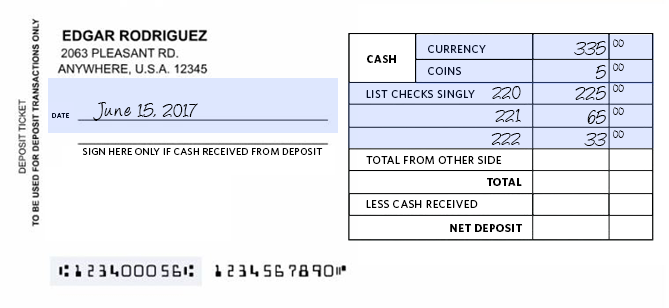

Checks List

If you are depositing a check, write the check number for the top right corner of the check.

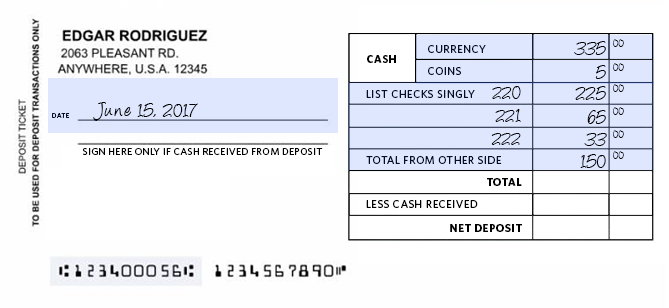

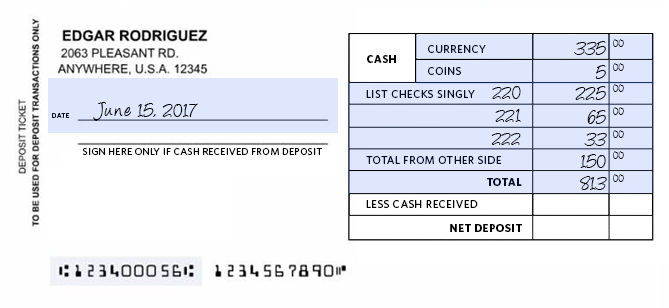

Total From Other Side

If you are depositing more checks than can be listed on the front, continue to list them on the back and write the total amount of the checks from the back side here.

Less Cash Received

If you would like the bank teller to give you cash back from your deposit, insert that amount in this field.

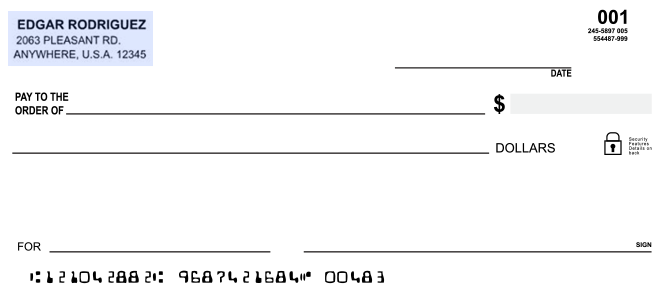

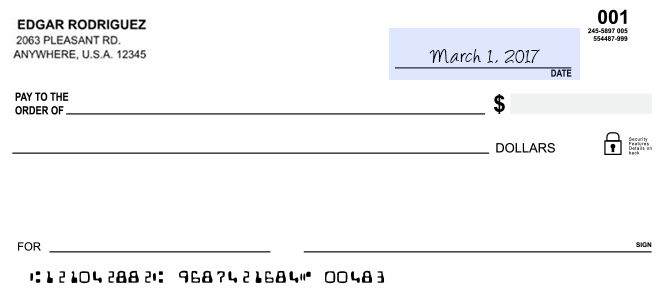

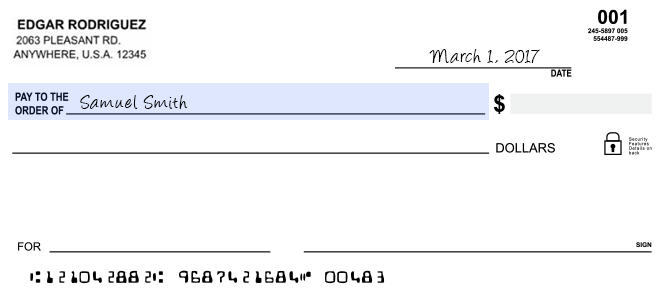

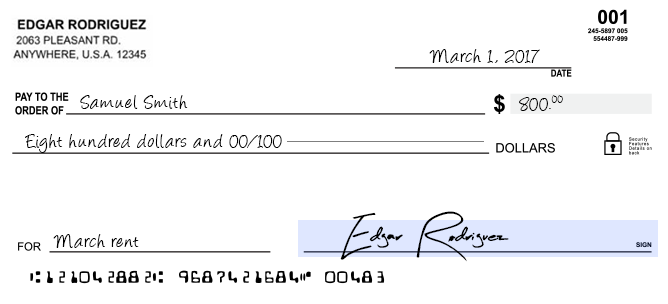

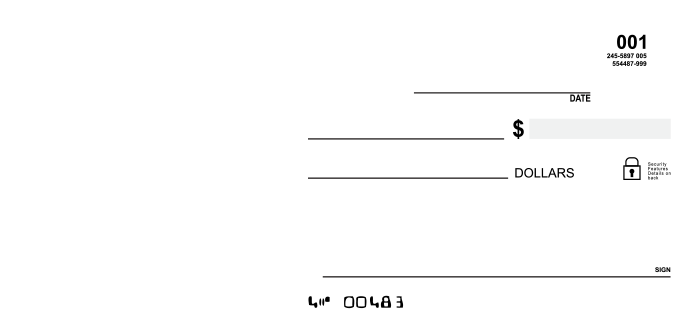

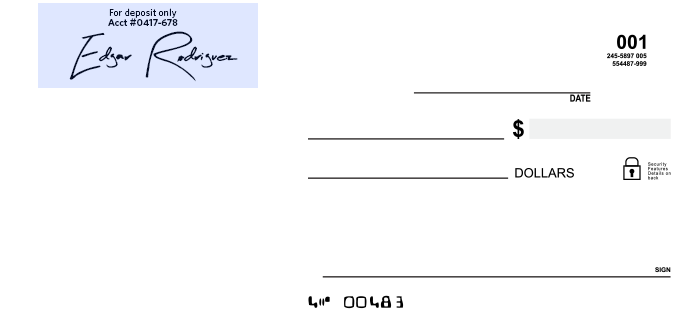

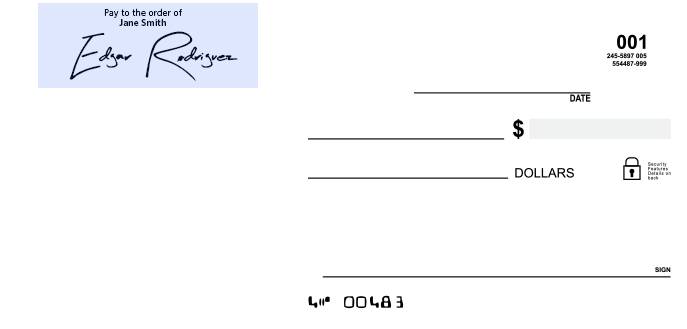

Name

Your personal information is printed here. Never list your social security number on your printed checks.

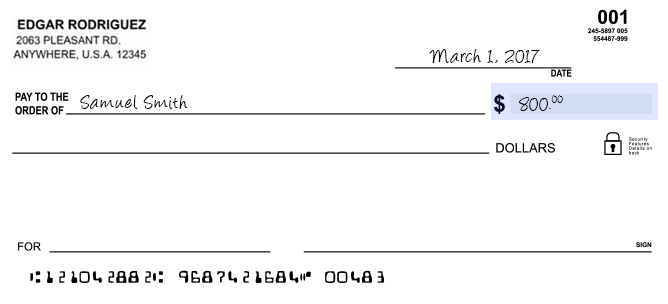

Check Amount in Numbers

Write the amount of the check numerically. Do not leave any space before the check amount where extra digits could be inserted.

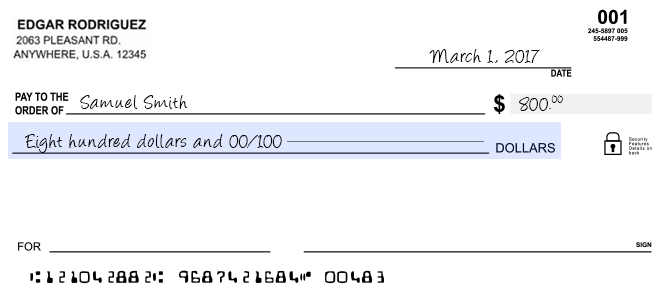

Check Amount in Words

Starting at the far left side of this field, write the check amount in words. follow the dollar amount with the word "and" before writing the amount of cents over 100 in the form of a fraction. Draw a line from there to the end of the field.

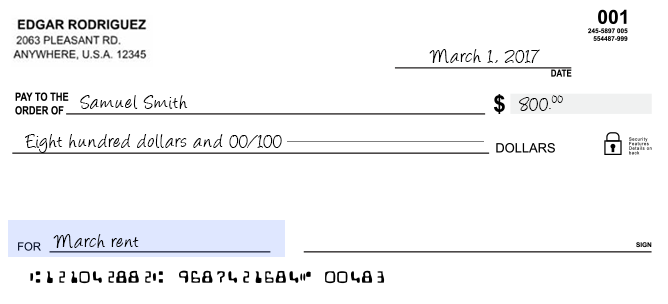

Memo

Use this space to note the purpose of the check. If you are paying a bill, you might wish to put your account number here.

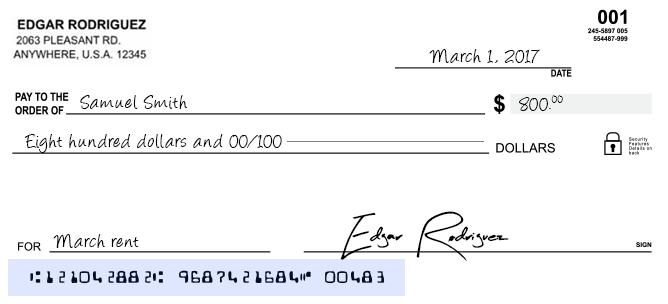

Identification Numbers

These numbers are used to identify the bank, your account number and the check number. They are printed in special magnetic ink that machines can read.

Endorsing a Check

Signing the back of a check is called "endorsing" the check. There are three ways to endorse a check.

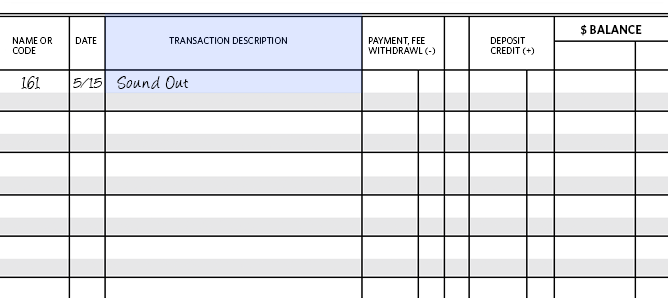

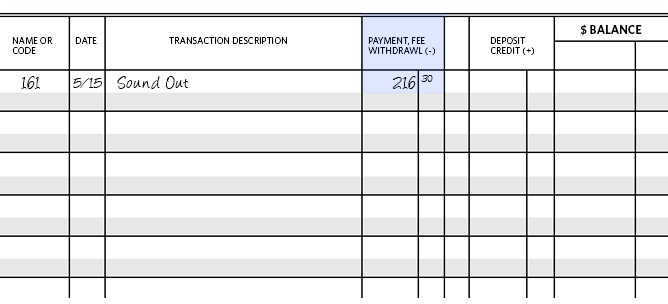

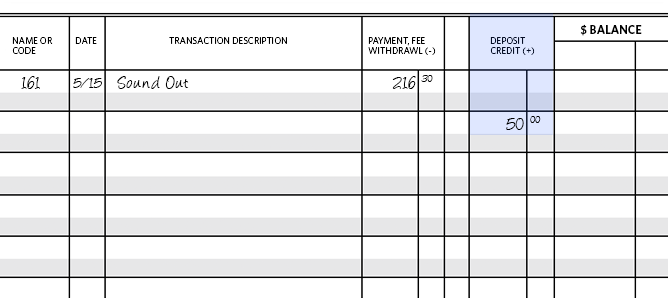

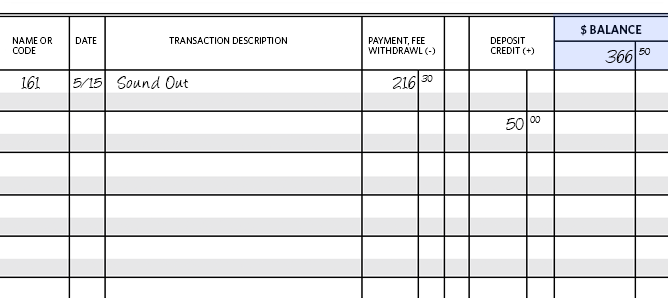

Transaction Register

Use a transaction register to keep track of payments (by check or debit card) or deposits you make in your account.

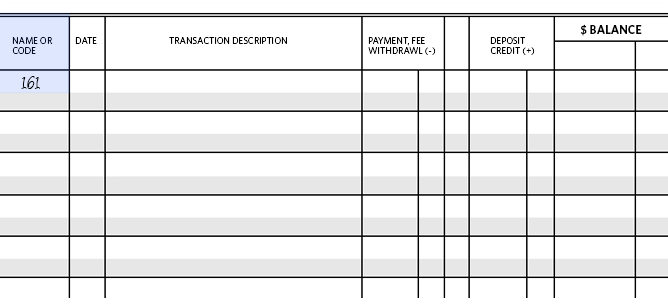

Starting Balance

Record your starting account balance here. When the page is full, carry the bottom balance oer to the starting balance on the next page.

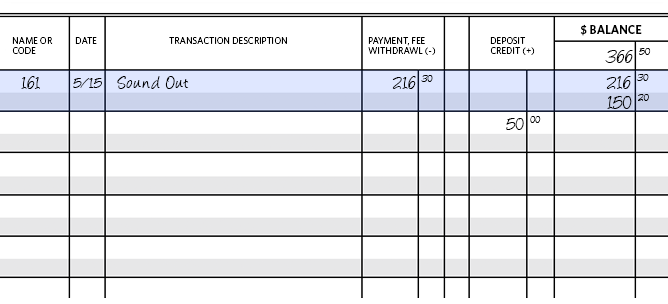

Recording a Check

Record the check number, date, to whom the check was written, the amount of the check and the reason the cehck was written. Subtract the amount of the check from your balance and write in the new balance.

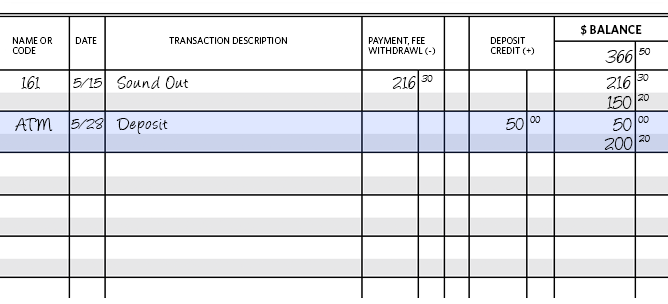

Recording a Deposit

Record the code, date, description and the amount of the deposit. Add the amount of the deposit to your balance and write in the new balance.

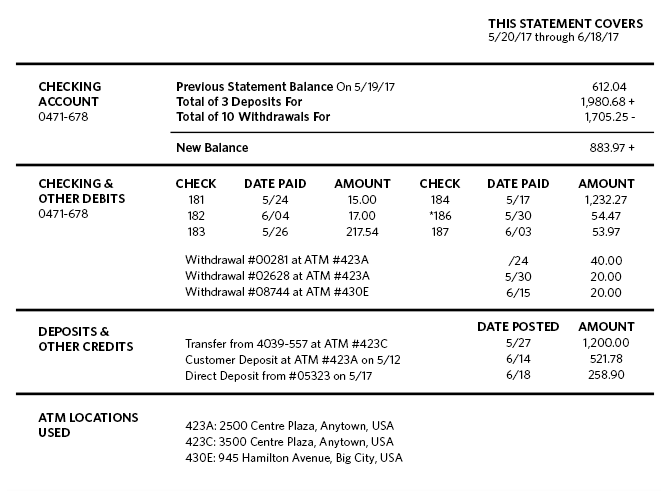

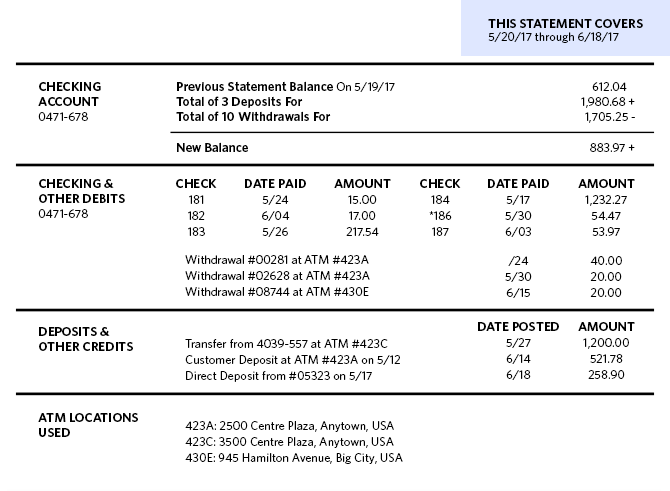

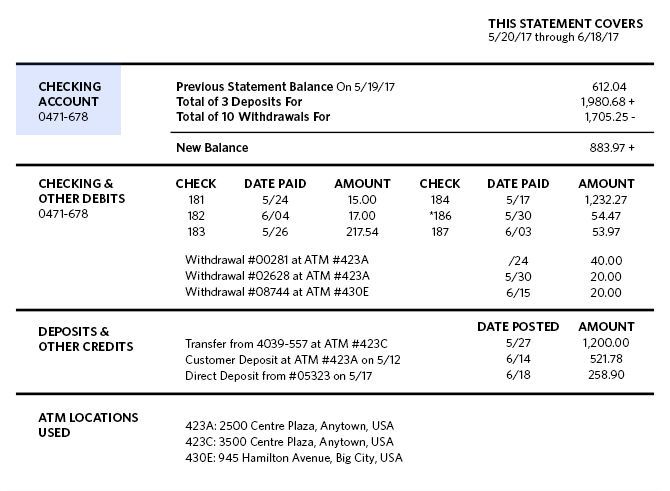

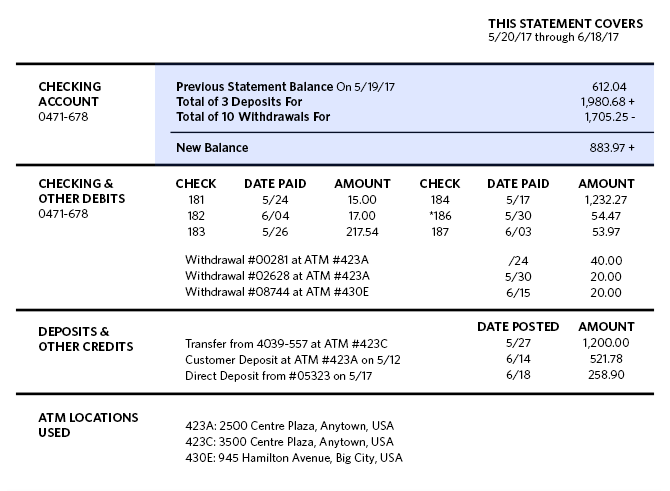

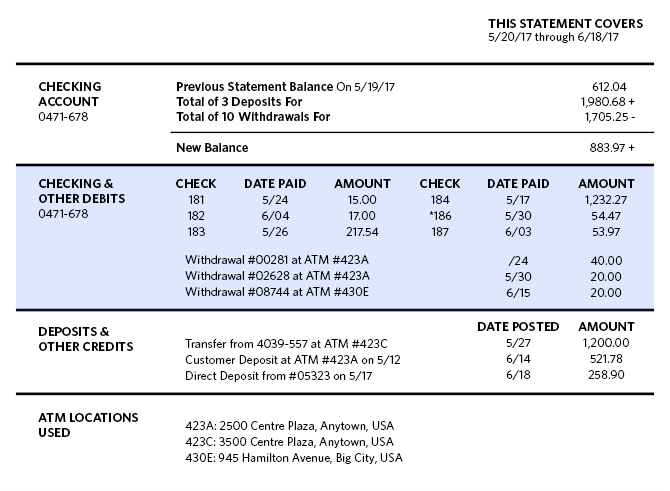

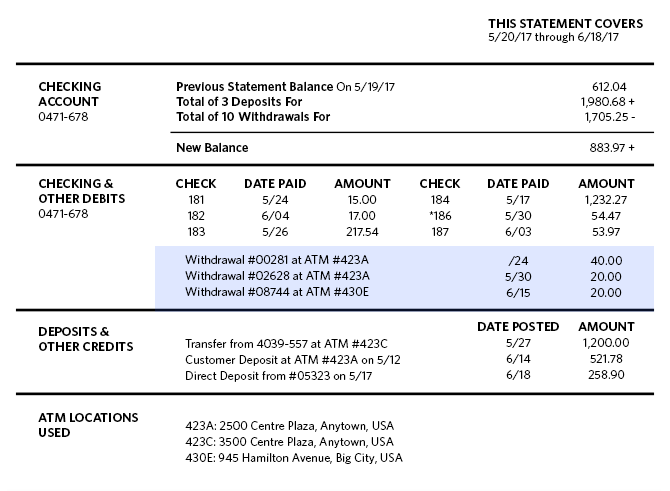

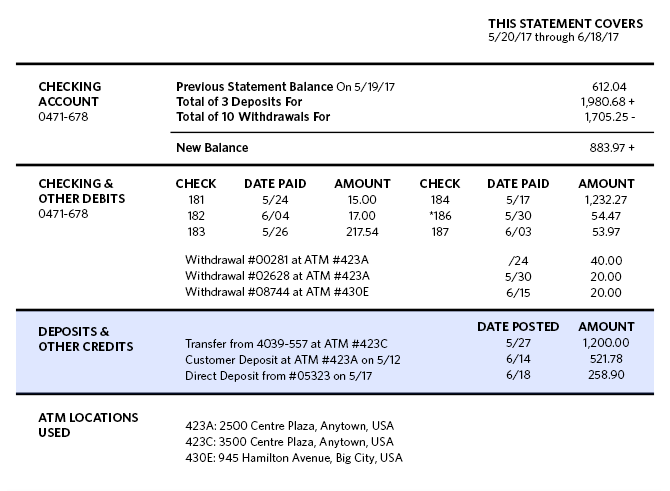

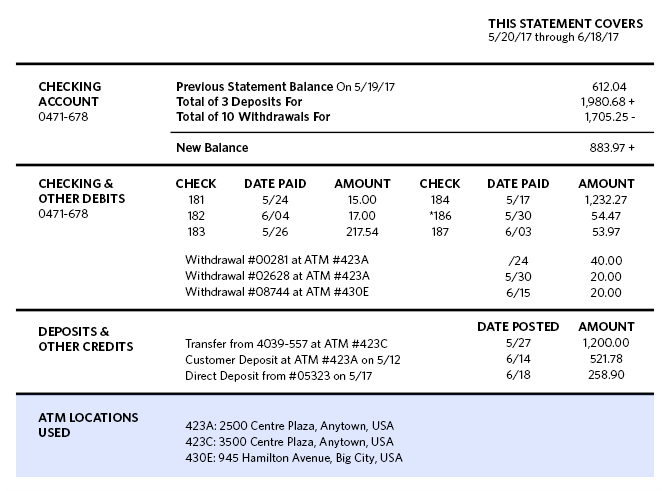

Reading a Bank Statement

To keep track of where your money goes and how much you have, it's important to know how to read a bank statement. This explains the information it contains.

Account Summary

This area displays your previous balance, total deposits, total withdrawals and your new balance.

Checks and Other Debits

This section lists all transactions in which money was withdrawn from your account.

Deposit and Other Credits

This section lists all transactions in which money has been deposited in your account.

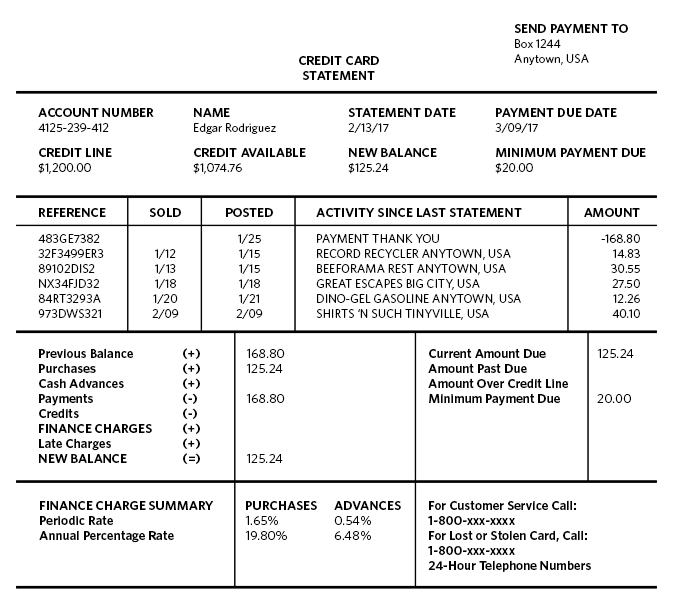

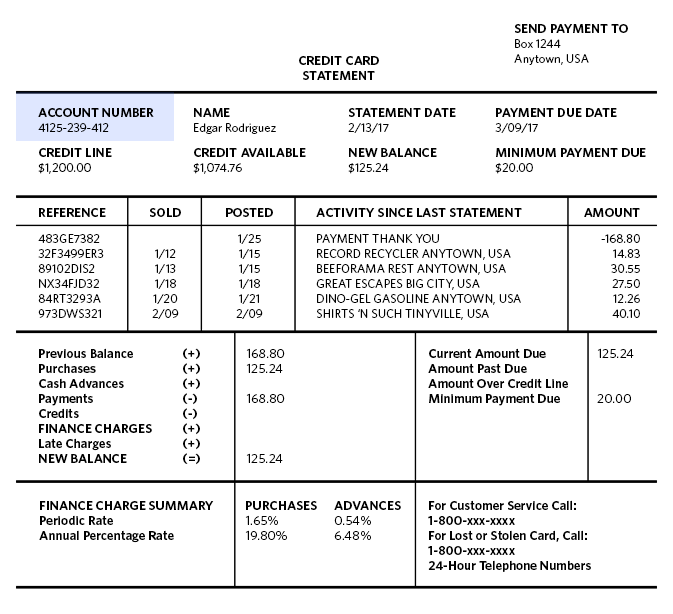

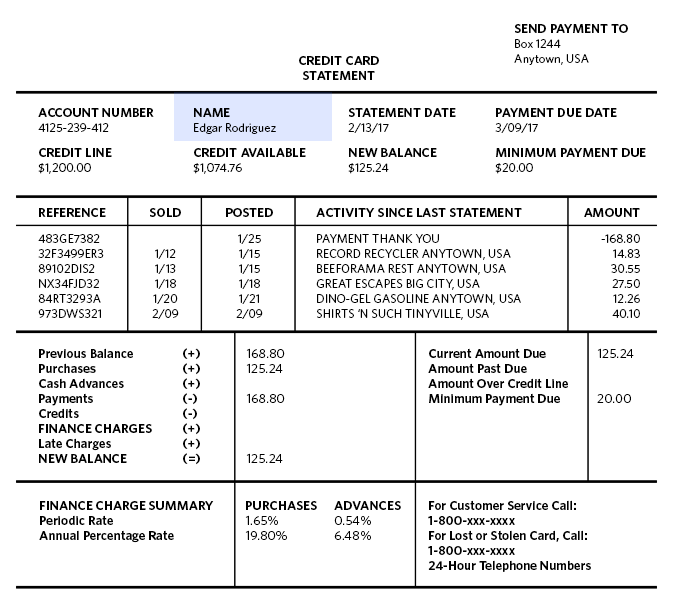

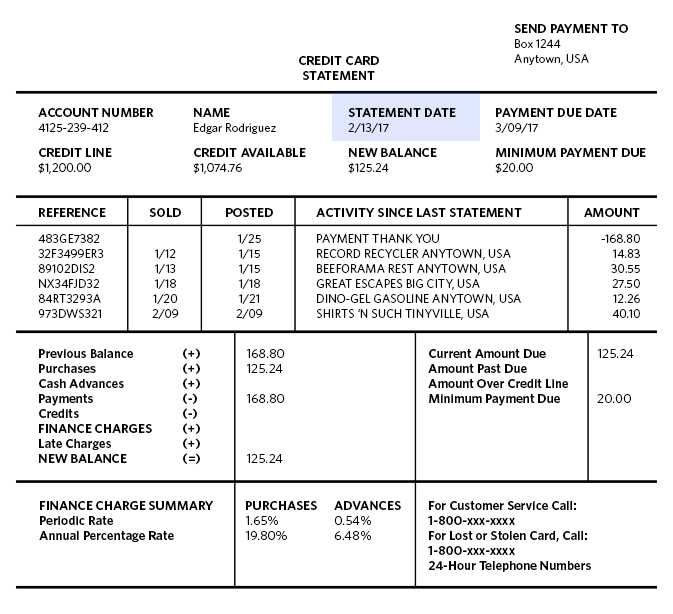

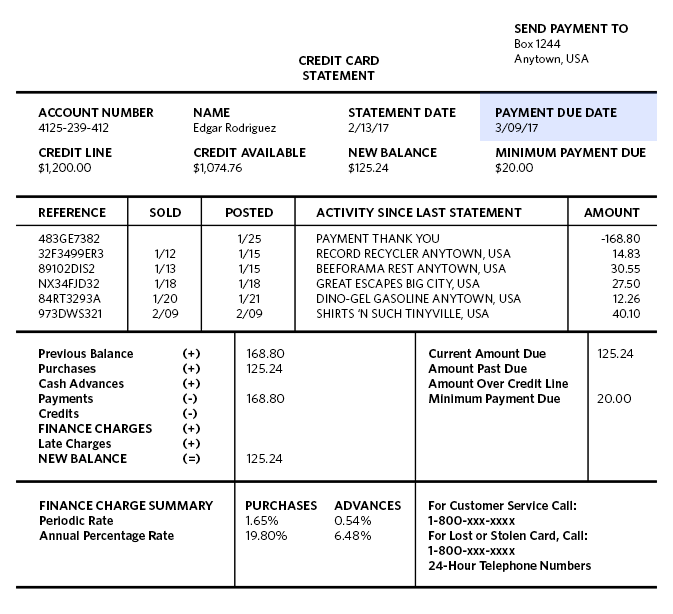

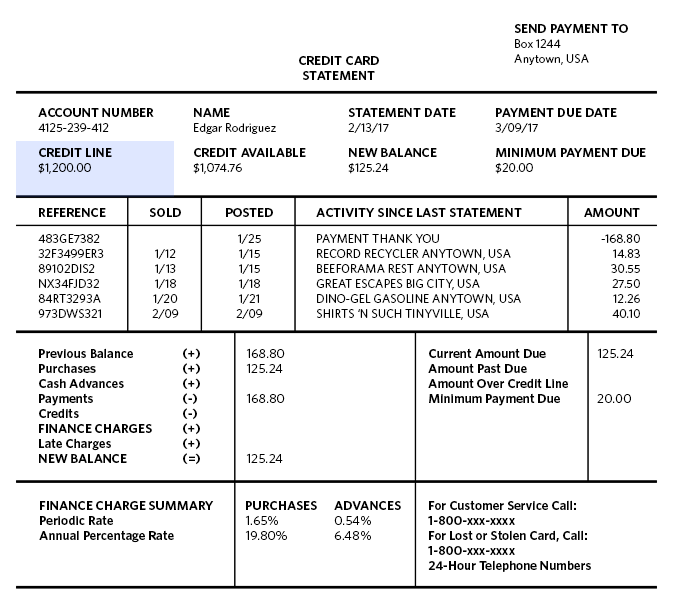

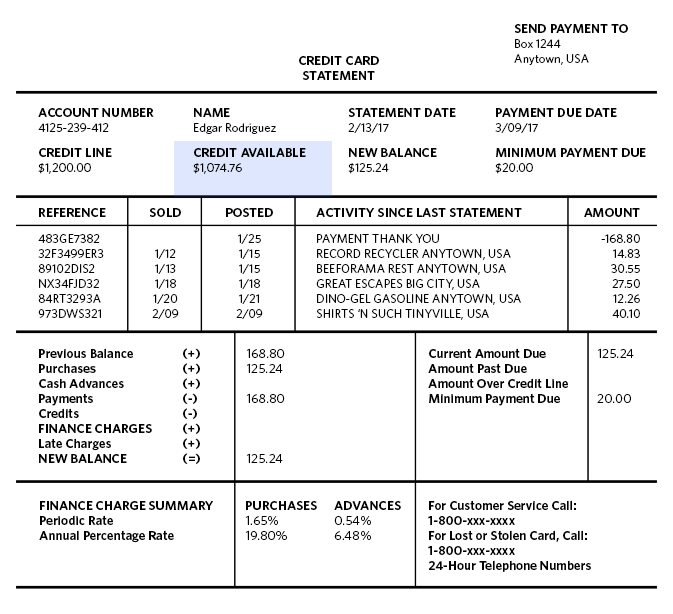

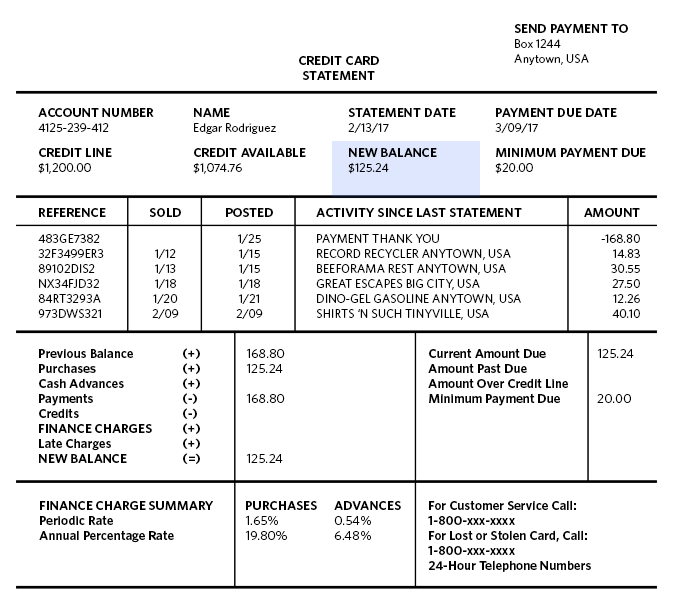

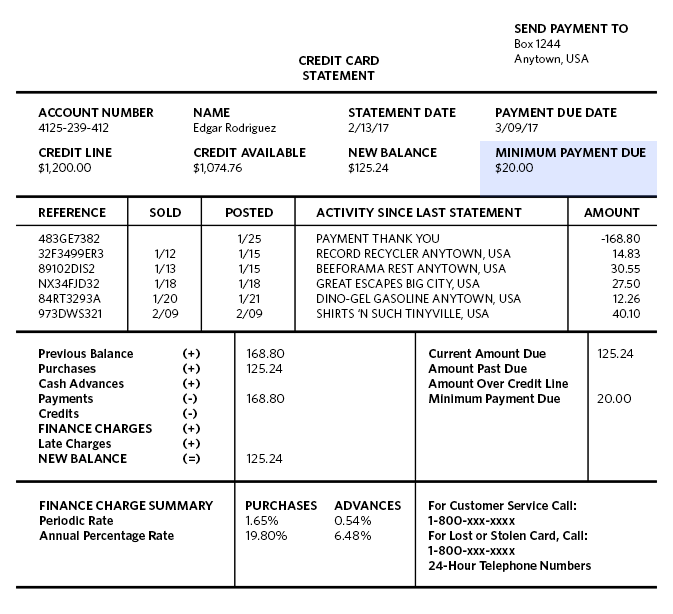

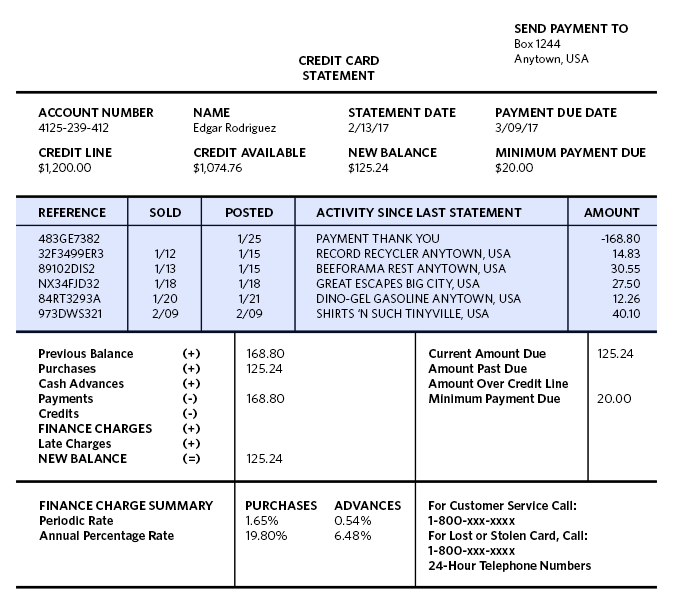

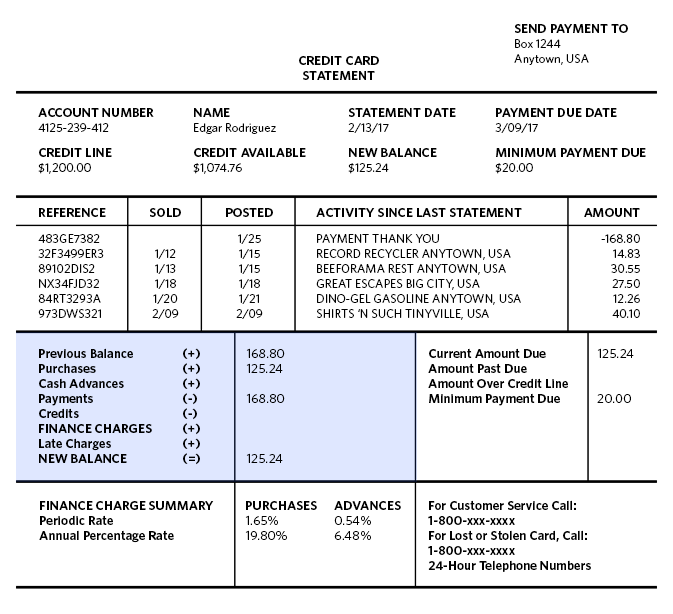

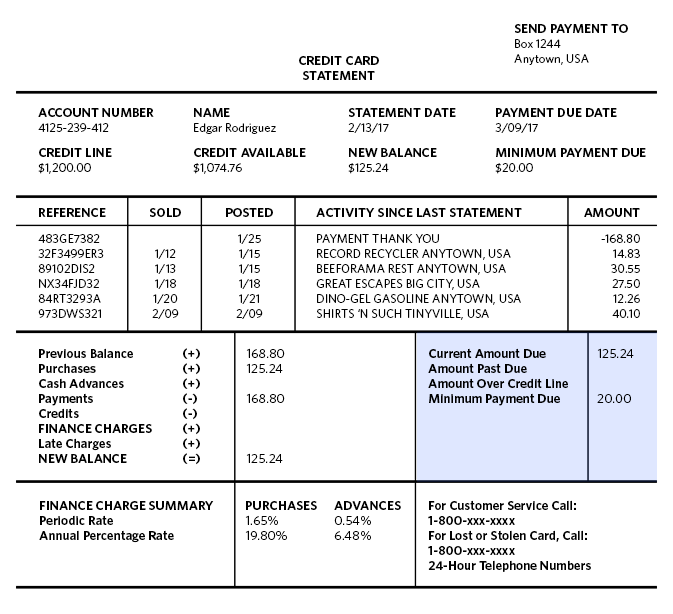

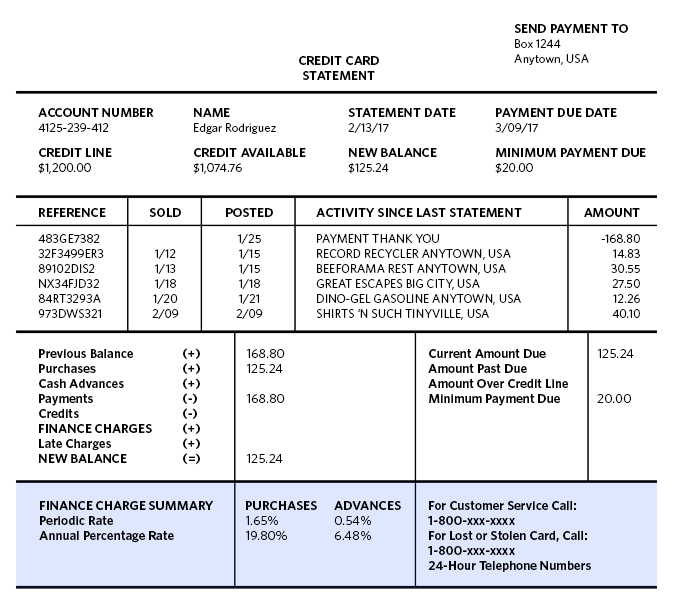

Reading a Credit Card Statement

Learning how to read your credit card statement will help you to effectively manage your credit usage.

Statement Date

All transactions occurring between the last statement date and this date appear on this statement.

New Balance

This is the current balance you owe on the card. You can pay the full amount and pay no interest. You can also pay a lesser amount and pay interest.

Transaction List

This area lists all the transactions you've made during the statement period. It includes perchases, returns, payments and interest charges.

Payment Information

This section shows your current balance, if there is any remaining balance from past statements, if you've spent past your credit limit and the minimum amount you must pay.

Compartir